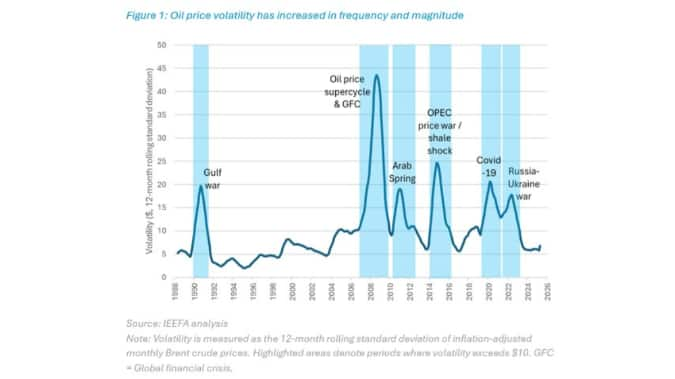

The disruption of the Strait of Hormuz has once again exposed a structural vulnerability in the global energy system. This is the second major fossil fuel shock in four years, following the outbreak of the Russia-Ukraine war. These crises are often framed as isolated incidents; in reality, they reflect a system built on volatile supply.

From Oil Tanker to Global Portfolios

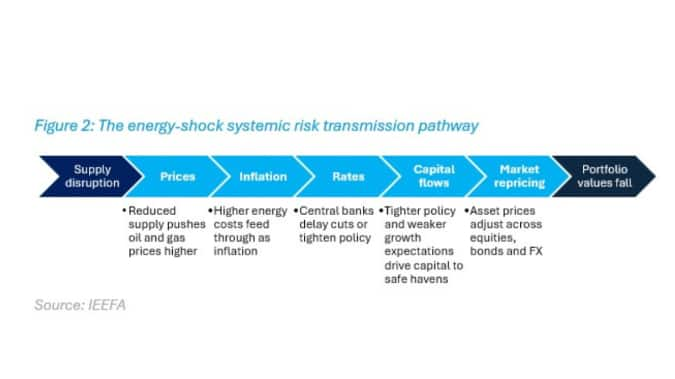

Energy shocks quickly move beyond local energy markets. Higher oil and gas prices feed into global inflation, forcing central banks to delay or reverse rate cuts. Growth expectations soften and assets reprice across classes.

Localised disruptions propagate across the broader economy. Markets respond quickly as prices adjust, capital reallocates and portfolios reposition—contributing to long-term, systemic financial risk.

You Can’t Diversify Systemic Risk

Portfolio theory encourages diversification to hedge specific risk, but because exposures are broad by design, investors cannot meaningfully avoid risks that affect the system as a whole. Overweighted positions in energy stocks or defensive assets can cushion the blow at the margin, but the rest of the portfolio still re-rates.

Short-Term Relief Reinforces the Risks

In response to energy crises, governments step in to shield consumers from higher fuel costs, funnelling public capital away from clean alternatives. The International Monetary Fund (IMF) projects global fossil fuel subsidies will rise to over USD 8 trillion by 2030. This response is understandable in isolation, but in a world of persistent shocks it is self-defeating. Short-term stabilisation measures only temporarily conceal an underlying structural vulnerability.

Cost Curves Alone Can’t Break the Cycle

The economics of clean energy and the availability of capital to deploy it are different problems. Wind, solar and battery costs have fallen sharply, but cheaper technology does not automatically solve financing constraints. Reducing exposure to volatile fossil fuels requires renewables to not only meet new demand, but also to displace existing fossil use. When financing conditions tighten, that shift slows and fossil dependence persists. Renewables are particularly sensitive to this given their high upfront costs.

Uneven Exposure to Energy Price Risk

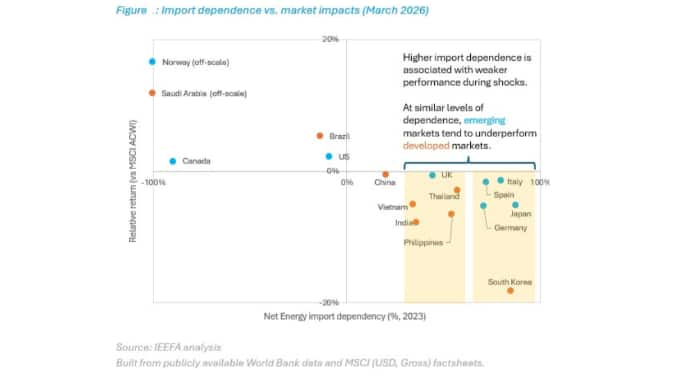

The global nature of these shocks does not mean the impact is evenly distributed. Many emerging markets remain heavily reliant on imported fossil fuels and energy shocks trigger a second-order effect that disproportionately affects them. India, for example, imports close to 89% of its crude oil, and Bangladesh, India, and Pakistan together import almost two-thirds of their LNG via the Strait of Hormuz.

As risk rises, institutional capital retreats from higher-risk emerging markets to safer havens. During the latest episode, MSCI's emerging market equities index lost more than USD 1 trillion in market capitalisation in a week as capital rotated out.

That capital flight only exacerbates the problem, driving currency depreciation and higher borrowing costs. The cost of capital in emerging markets is already significantly higher than in developed markets, but during periods of stress that gap widens further. Capital-intensive clean energy becomes harder to finance at precisely the moment it becomes most urgent. The result is a self-reinforcing loop in which countries most exposed to fossil fuel volatility are also least able to finance their way out of it.

Clean Energy in Emerging Markets: Managing Portfolio Risk

Much of the growth in energy demand over the coming decades will come from emerging markets. Meeting that demand through fossil fuels will only increase pressure on a supply base that is prone to disruption. Risks will transmit more forcefully across the global economy—not just where the demand originates.

For investors and policymakers in developed markets, this is not a peripheral issue. Allocating capital to clean energy in emerging markets is not only about development or climate targets, but it also directly affects the stability of the global system their portfolios and economies depend on.

Reducing Risk, Not Reacting to It

Fossil-driven volatility is a recurring, systemic feature and policy and investor responses need to reflect that.

· Treat clean energy as risk management

Investors should factor energy import dependence and fossil fuel volatility into wider country risk, asset allocation and stewardship frameworks. Through sovereign engagement, they can encourage policies that reduce exposure to volatile fossil fuel imports and support clean energy, grids and electrification in fossil fuel-importing markets.

· Keep capital available as risks rise

Emerging markets face a structural financing gap projected to reach USD 2.4 trillion annually by 2030. Guarantees, concessional capital and blended finance structures should be used to keep viable clean energy projects moving during periods of stress, rather than allowing capital flight to reinforce dependence on fossil fuels.

Build investable pipelines, not just ambition.

Capital will not move at scale without bankable projects, stable regulation and structures that meet institutional investor requirements. Governments, DFIs and investors should work together on project preparation, grid investment and currency-risk mitigation so clean energy targets become investable opportunities.